The equity market continued its strong upward trajectory in May, adding nearly GH¢91billion in market value over the past year as declining inflation, lower interest rates and rising investor participation reinforced one of the strongest stock market rallies in recent history.

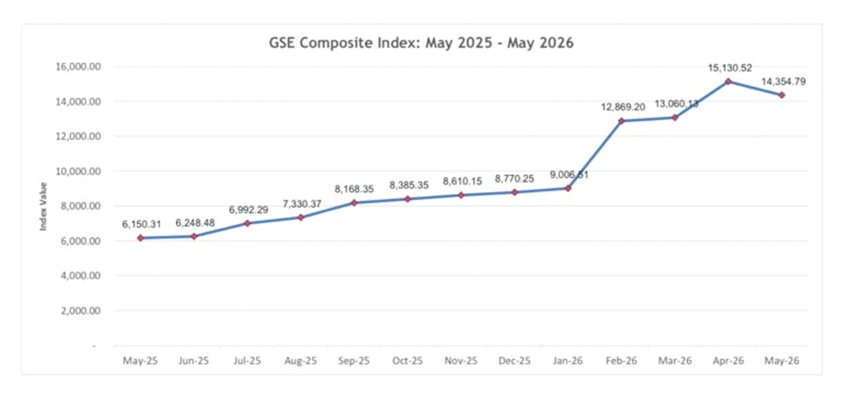

The Ghana Stock Exchange’s (GSE) market capitalisation rose to GH¢262.95billion in May, representing a year-to-date increase of 52.84 percent while the benchmark GSE Composite Index (GSE-CI) climbed 63.67 percent to 14,354.79 points.

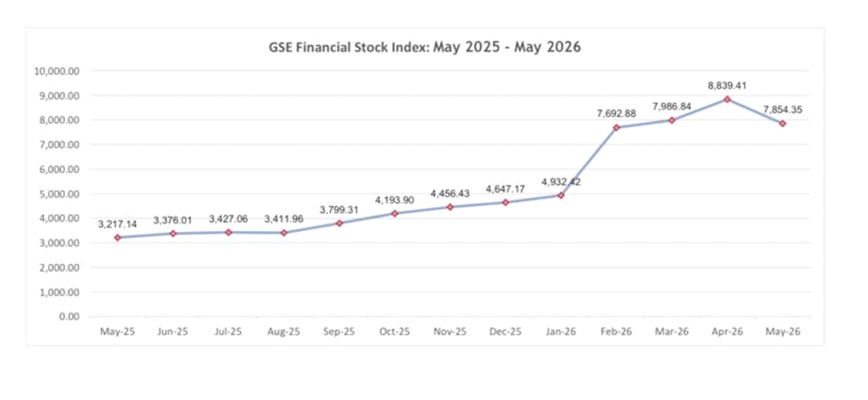

The GSE Financial Stocks Index (GSE-FSI) gained 68.99 percent to 7,854.35 points, extending a rally driven largely by banking, telecommunications, insurance and energy stocks.

The gains come as investors increasingly rotate away from fixed-income instruments following a sharp decline in Treasury bill yields and inflation. Consumer inflation stood at 3.7 percent in May from 18.4 percent a year earlier, while yields on the 91-day, 182-day and 364-day Treasury bills fell to 4.99 percent, 7.04 percent and 10.46 percent respectively.

The macroeconomic environment’s shift has improved the relative attractiveness of equities, prompting both institutional and retail investors to increase exposure to listed stocks.

Trading activity reflected that growing appetite. Total traded volume rose 168.5 percent year-on-year to 92.74 million shares in May, while transaction volumes surged 347.1 percent to 89,945 trades. The value of shares traded increased 32.7 percent to GH¢247.61million.

Year-to-date, investors traded 716.25 million shares worth GH¢3.41billion – representing increases of 503.2 percent and 323.6 percent respectively compared with the same period in 2025.

The marked increase in transactions points to participation gradually broadening beyond the market’s traditional institutional base.

According to investment advisory firm EcoCapital, the rise in trading activity reflects a combination of long-term investment positioning and short-term tactical trading as investors respond to changing market conditions.

The firm said some investors continue to accumulate equities they consider undervalued relative to future earnings potential, while others are taking advantage of momentum-driven gains and market volatility.

“Overall, I believe the broader trend suggests growing confidence in equities as an asset class again. Investors are becoming more willing to take calculated risks as macroeconomic conditions improve,” EcoCapital Chief Executive Dela Agbo said in an interview response with B&FT.

Despite the increase in participation, market liquidity remains heavily concentrated in a small number of stocks.

MTN Ghana accounted for approximately 80 percent of total market value traded during May and nearly 79 percent of cumulative market value traded during the first five months of the year, reinforcing its role as the market’s dominant liquidity anchor.

Other actively traded counters included GCB Bank, Ecobank Transnational Incorporated, CAL Bank, Societe Generale Ghana, Zenith Petroleum Holdings and GOIL.

Analysts say the concentration creates efficient trading opportunities but also exposes the market to risks associated with dependence on a handful of large-cap stocks.

Financial stocks remain at the centre of the rally. Banking shares have benefitted from lower interest rates, improving asset quality, stronger earnings and recovering investor confidence following the sector’s adjustment to the Domestic Debt Exchange Programme (DDEP).

Several banks – including GCB Bank, Access Bank, CAL Bank, Republic Bank Ghana, Ecobank Transnational Incorporated and Societe Generale Ghana – have recorded significant gains this year.

Databank Asset Management said in its equity market review that the financial sector’s recovery has been reinforced by dividend reinstatements and improving balance sheet strength. The firm noted that banks are increasingly moving beyond capital preservation toward earnings growth and capital deployment after two years of post-DDEP rebuilding.

The insurance sector has also emerged as a major beneficiary of renewed investor interest. Enterprise Group and SIC Insurance have posted substantial gains amid improving profitability and growing demand for non-bank financial stocks.

Meanwhile, energy-related counters such as GOIL and ZEN Petroleum have attracted investor attention on expectations of stronger earnings growth and expansion opportunities within the downstream petroleum sector.

Market breadth remains strong despite recent profit-taking. Among the strongest-performing stocks this year are Clydestone Ghana, SIC Insurance, Republic Bank Ghana, Enterprise Group, GOIL, Standard Chartered Bank Ghana, Cocoa Processing Company, ZEN Petroleum and Guinness Ghana Breweries.

Databank reported that 22 stocks advanced during the first quarter against only one decliner, reflecting broad-based participation across the financial, consumer, telecommunications and energy sectors.

The rally’s strength has positioned Ghana among the best-performing equity markets in Africa.

Market Analyst at Fincap Securities John Nani estimates the Ghana market generated returns of approximately 60.95 percent in U.S. dollar terms by the end of April, trailing only Nigeria among major frontier and emerging African markets. This performance significantly exceeded returns recorded in Egypt, Kenya, Tunisia and South Africa.

Analysts attribute the outperformance partly to a re-rating of stocks that had previously traded at depressed valuations during Ghana’s macroeconomic and debt restructuring challenges.

While investor sentiment remains positive, market participants are increasingly focused on sustainability.

Recent weakness in financial stocks has prompted concern among some investors, although analysts broadly view the development as a normal correction following an exceptionally strong rally.

EcoCapital described the recent sell-off of banking stocks as a recalibration rather than loss of confidence, driven largely by profit-taking, portfolio rebalancing and investor caution over the sustainability of earnings growth.

The firm noted that investors are becoming more selective, focusing increasingly on earnings quality, governance standards and long-term growth prospects rather than momentum alone.

Primary market revival gathers pace

The rally is also beginning to influence corporate fundraising activity. According to Fincap Securities, stronger secondary-market valuations are improving confidence among potential issuers. ZEN Petroleum recently raised GH¢640million through an IPO that reportedly attracted bids of approximately GH¢970million.

Kasapreko’s GH¢700million offer provided an even sharper demonstration of demand. The beverage manufacturer attracted subscription requests worth nearly GH¢1.73 billion, more than twice the amount it sought to raise, with 18,781 qualified applicants seeking approximately 1.44billion shares against the 583.3million available. The 146 percent oversubscription forced the company to allocate shares at a uniform rate of 40.56 percent across all investor categories.

The participation figures point to one of the broadest retail and institutional investor turnouts seen on the GSE in recent years, with both domestic and foreign investors competing for allocations.

Data released by the company showed that local institutional investors dominated demand, accounting for bids of more than 1.08billion shares, or roughly three-quarters of total subscriptions. Local individual investors made a strong showing with applications for over 189million shares, while foreign institutional and individual investors collectively bid for more than 162 million shares.

The strong institutional participation underscores growing confidence among professional investors in consumer-focused businesses with established brands and regional growth ambitions, while the large number of individual investors reflects increasing public interest in equities as declining interest rates encourage diversification beyond traditional fixed-income assets.

Market observers say the breadth of participation is significant because it demonstrates the ability of Ghanaian companies to mobilise long-term capital from a wide investor base through the stock market.

Kasapreko’s Board Chairman, Samuel Leslie Adetola, described the response as a vote of confidence in the company’s future prospects and in Ghana’s capital markets.

For Kasapreko, best known for its Alomo Bitters brand, the successful fundraising provides capital to expand production capacity and accelerate international growth plans. The company is scheduled to begin trading on the GSE on June 15 under the ticker symbol KASA, and market participants will be watching closely to see whether the strong demand recorded during the offer period translates into sustained trading activity once the shares debut.

For the market, the transaction may prove equally important as a test of investor demand for new listings. Analysts say sustained momentum could encourage additional listings, corporate bond issuances and broader use of capital markets financing by indigenous businesses.

Outlook

Most market participants expect the pace of gains to moderate during second-half 2026, although the broader upward trend is expected to remain intact.

Databank forecasts the GSE Composite Index could end the year around the 16,000-point level, supported by continued economic recovery, earnings growth and investor demand for dividend-paying stocks.

However, analysts caution that risks remain. Potential threats include a resurgence in inflation, which has already gone up twice and was at 3.7 percent as of May 2026; exchange-rate volatility, at about 11 percent depreciation year to date against the US dollar; fiscal slippages, external financing pressures and higher global oil prices, which remained elevated at about US$90/bbl. Databank also warned that escalating geopolitical tensions could affect foreign exchange inflows, raise imported inflation and weaken growth momentum.

Nonetheless, lower inflation, lower interest rates, improving corporate profitability and rising investor participation continue to provide support for equities. Entering second-half of the year, investors are expected to become more selective – but analysts broadly agree that the equity market remains in a cyclical bull phase, with fundamentals continuing to favour stocks over most domestic fixed-income alternatives.